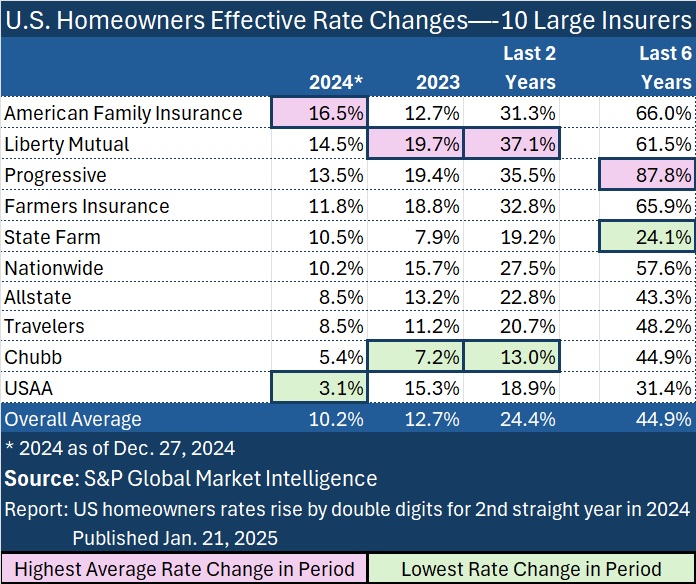

Based on a brand new evaluation of householders insurance coverage charges, some Midwest states noticed the largest jumps in premiums final 12 months—and American Household Insurance coverage topped a listing of 10 insurers ranked by common fee change.

The evaluation revealed by S&P World Market Intelligence this week is predicated on householders fee filings accepted via Dec. 27, 2024—so not fairly the entire 12 months final 12 months.

Based on S&P GMI, the calculated weighted nationwide common efficient fee enhance for householders insurance coverage was 10.4% final 12 months via late December. In 2023, the comparable determine was 12.7%, placing the two-year common enhance at roughly 24 %.

{kind=link}

The state for which S&P GMI calculated the largest efficient fee will increase for 2024 was Nebraska with 22.7%. In whole, 33 states had double-digit calculated efficient fee will increase final 12 months, with charges in Montana, Iowa, Minnesota, Utah and Washington additionally rising greater than 20% by S&P GMI’s calculations.

Minnesota and Iowa have been additionally among the many states with the best direct loss ratios in 2023 (together with protection prices), though Hawaii, Kentucky and Arkansas have been worse.

On the opposite finish of the spectrum, Florida had the bottom—at 1.0%—however the textual content of the report notes that Florida’s calculation doesn’t embrace any modifications by Residents Property Insurance coverage Corp., the state-backed insurer of final resort.

For American Household, which raised charges in 42 states final 12 months, the service’s three largest weighted-average fee will increase occurred in Missouri (30.1%), Illinois (27.5%) and Nebraska (27.1%), the S&P GMI report says.

Concerning the Evaluation

Fee submitting data for S&P GMI’s evaluation was sourced from System for Digital Fee and Kind Submitting paperwork and is restricted to owner-occupied householders fee filings of every state’s 10 largest house owner underwriters primarily based on 2023 direct premiums written plus any of the nation’s 10 largest house owner underwriters exterior the state’s high 10, excluding state-backed insurers of final resort like Residents Property Insurance coverage Corp. of Florida in addition to mobile houses, rental and apartment strains of enterprise.

The calculations are primarily based on fee filings entered into the database via Dec. 27, 2024, for 49 states plus the District of Columbia. Wyoming was excluded as a result of a restricted variety of fee filings.

Whereas the Wisconsin-based mutual insurer pushed charges up greater than 31%, on common, countrywide within the final two years, the most important house owner insurer, State Farm, ranks in the midst of the pack by way of fee hikes with a two-year common enhance of lower than 20% throughout all states.

The truth is, whereas the ten insurers analyzed by S&P GMI elevated householders charges by about 45% over the six-year interval from 2019-2024, State Farm scored the bottom six-year soar at 24%.

One other mutual, Liberty Mutual, applied the second-highest weighted-average fee change calculated by S&P GMI throughout the nation, at 14.5% in 2024, and the most important two-year soar (of about 37%).

The textual content of the S&P GMI report offers extra details about the states wherein Liberty Mutual, Progressive and Farmers boosted charges essentially the most, and features a state-by-state chart itemizing general common fee modifications for the ten insurers mixed for every of the years 2019-2024.

Profitability Improves

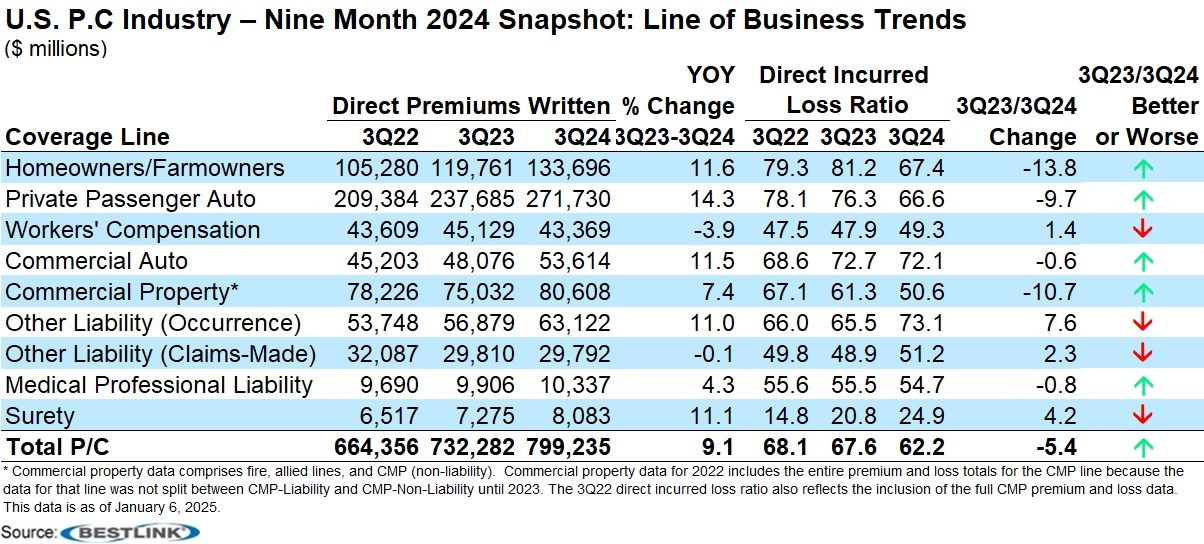

Individually, score company AM Finest revealed an evaluation of loss ratio modifications by line via the primary 9 months of 2024, discovering that householders was essentially the most improved line, pushed by an aggressive push for charges.

Total, the householders loss ratio skilled a 13.8-point enchancment through the first 9 months of 2024, in comparison with the identical interval in 2023, in accordance with the report titled “3Q24 Snapshot: Private Strains Propels Enchancment in Direct P/C Trade Underwriting Outcomes, which summarizes knowledge derived from U.S. P/C carriers’ third-quarter statutory statements (obtained and aggregated as of Jan. 6, 2025).

Throughout all strains, the loss ratio dropped 5.4 factors, and AM Finest mentioned the considerably improved direct underwriting outcomes have been pushed by elevated earned premiums, which have outpaced the rise in incurred loss and loss adjustment bills, and different underwriting bills.

“The non-public strains phase noticed essentially the most notable enchancment, benefiting from an aggressive push for extra ample charges, pricing segmentation in private auto, the affect of underwriting initiatives and improved disaster danger administration practices,” AM Finest mentioned, noting that the advance for the householders line got here despite Hurricane Helene, which impacted third-quarter outcomes.

David Blades, affiliate director, Trade Analysis and Analytics, AM Finest, famous that though the nine-month outcomes present “optimism for full-year direct and web outcomes, Hurricane Milton, which occurred within the fourth quarter, is predicted to have a larger affect on householders and business property outcomes than Helene.”

Business property was the second-most improved line by way of underwriting revenue, with the loss ratio for that line dropping 10.7 factors.

Shut behind, the non-public auto phase’s direct loss ratio via third-quarter 2024 improved by practically 10 proportion factors and skilled an industry-leading 14% enhance in direct premiums written.

Direct premiums written throughout the property/casualty {industry} have been up by 9.1% in contrast with the identical interval in 2023, barely beneath the ten.2% enhance via third-quarter 2023.

Earlier this week, Vacationers, the primary publicly traded insurer to announce full-year earnings, reported elevated underwriting earnings for the corporate general, however the greatest mixed ratio enchancment was a ten.4 level year-over-year drop for its private insurance coverage phase (10.7 factors for householders and 10.0 factors for private auto).

Vacationers full-year mixed ratio for the householders line landed at 93.9, despite greater than 24 factors of disaster losses. The service reported renewal premium modifications averaging 14.1% within the fourth quarter of 2024.

Matters

Traits

Pricing Traits

Householders

{kind=link}